|

With the focus turned to DC and all things political this week, there is a distinct focus on the legislative and policy opportunities before us. US Rice Producers Association was in DC for our annual fly-in this week (more on that in today’s DC Update), and front and center of all conversations on the Hill was the Farm Bill. The House Agriculture Committee is expected to drop their version today, with markup coming later in the month. However, it will be a monumental lift for the Senate to get on board with it right now. For obvious reasons, passing an updated and modernized Farm Bill is of utmost importance to producers, who are facing extreme and unfair competition from governments that are highly subsiding their rice crops, thus distorting global trade. This isn’t the whole reason that milled and paddy exports are lagging significantly behind last year, down 12% and 49% respectively year over year, but this can certainly take some of the responsibility.

This will be the first week that we take a formal stab a predicting acreage for the coming year. We have been using a broad “30% reduction” for Long Grain acres; while that is likely true for Arkansas, some of the other states are looking going to be above and below that number as well. From our surveys, our best guess is that Arkansas will have 825,000 acres of long grain and 150,000 acres of medium grain, for a total of 975,000 acres. From the boots on the ground we’ve talked to, nobody is expecting acres to crest 1 million. In Louisiana, the crop is expected to be down about 13%; long grain acres at 375,000, medium grain at 50,000 acres, for a total of 425,000 acres. Mississippi is expected to be down by a whopping 35% to only 95,000 acres, and Missouri down 18% to 165,000 acres. Texas is also down significantly to only 115,000 acres, about a 20% drop. The only state that is expected to maintain its acreage is California, still north of 500,000 acres, perhaps equal to last year at 525,000 acres.

As of this date, surveys indicate total expected long-grain production for the 2026 season is 1.555 million acres. Last year, the country had a total of 2.118 million long grain acres, a difference of 563,000 acres, or a 27% reduction. It is staggering to expect more than 560,000 acres to not be planted into rice. One significant factor to note, however, is that we expect carry-in to remain at record highs, perhaps ending above 37 million cwt. The average carry-in over the last three years is 20 million cwt, or the equivalent of 265,000 acres. This means that additional 17 million cwt will “add” over 220,000 acres on top the short plant, thus extending the supply and perhaps muting any upwards price movement that could be expected to result from losing more than a quarter of the supply.

We will refine these numbers in the coming weeks, but quantifying the loss to over 560,000 long grain acres is a significant departure from the norm. As we have discussed previously, though, this reduction may help the market clear out old supplies and refine some of its processes to become more efficient and customer-centric in the coming marketing campaigns.

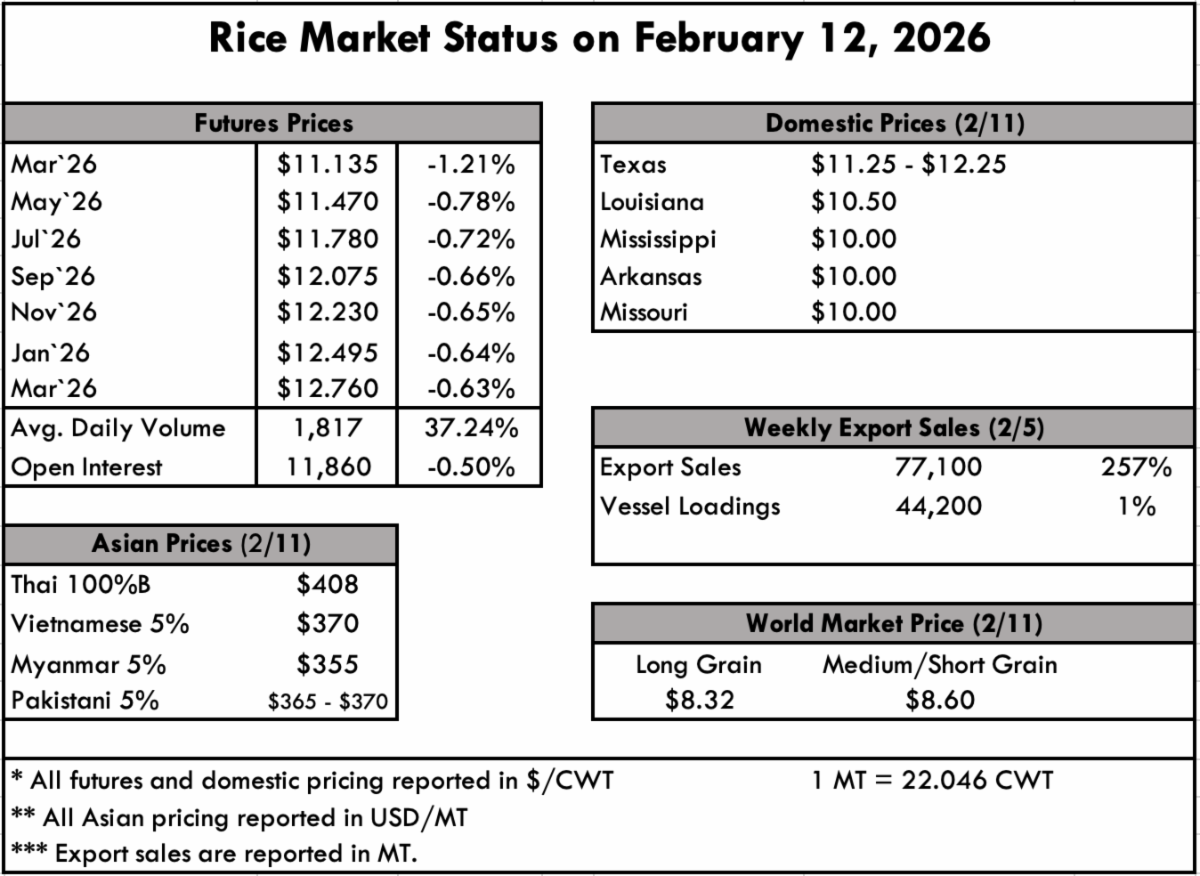

The weekly USDA Export Sales Report shows net sales of 77,100 MT this week, up noticeably from the previous week and up 61% from the prior 4-week average. Increases primarily for Colombia (27,500 MT) and Mexico (20,900 MT). Exports of 44,200 MT were up 32% from the previous week, but down 19% from the prior 4-week average.

We will have a thorough summary of the most recent WASDE report next week and its implications on the market.

|

")