|

Planting intentions are coming in to focus, as price action continues to move at a snail’s pace. In light of the recent strikes on Iran, the grains complex, and more specifically U.S. long grain prices, have not moved much—yet. It is still very early for there to be direct impacts from the war, but there are more subtle elements at work. First, in wartime, it is typical for the U.S. Dollar to increase in value against other global currencies as it is deemed safer than alternative global currencies. This, naturally, has a negative impact on exports. Secondly, and conversely, Iraq is one of the most strategic partners for milled U.S. long grain rice, and it’s typical for countries in conflict to stockpile basic food staples, of which rice is paramount. While there are only rumors of Iraq entering the conflict, it is something to watch. And third, what is making the news and directly impacting commodity and goods flow, is freight rates and the risk of shipping channels in the Middle East. This will have the most outsized impact short-term, but expect the first two factors to work their way into the matrix in the coming weeks if and when the war matures.

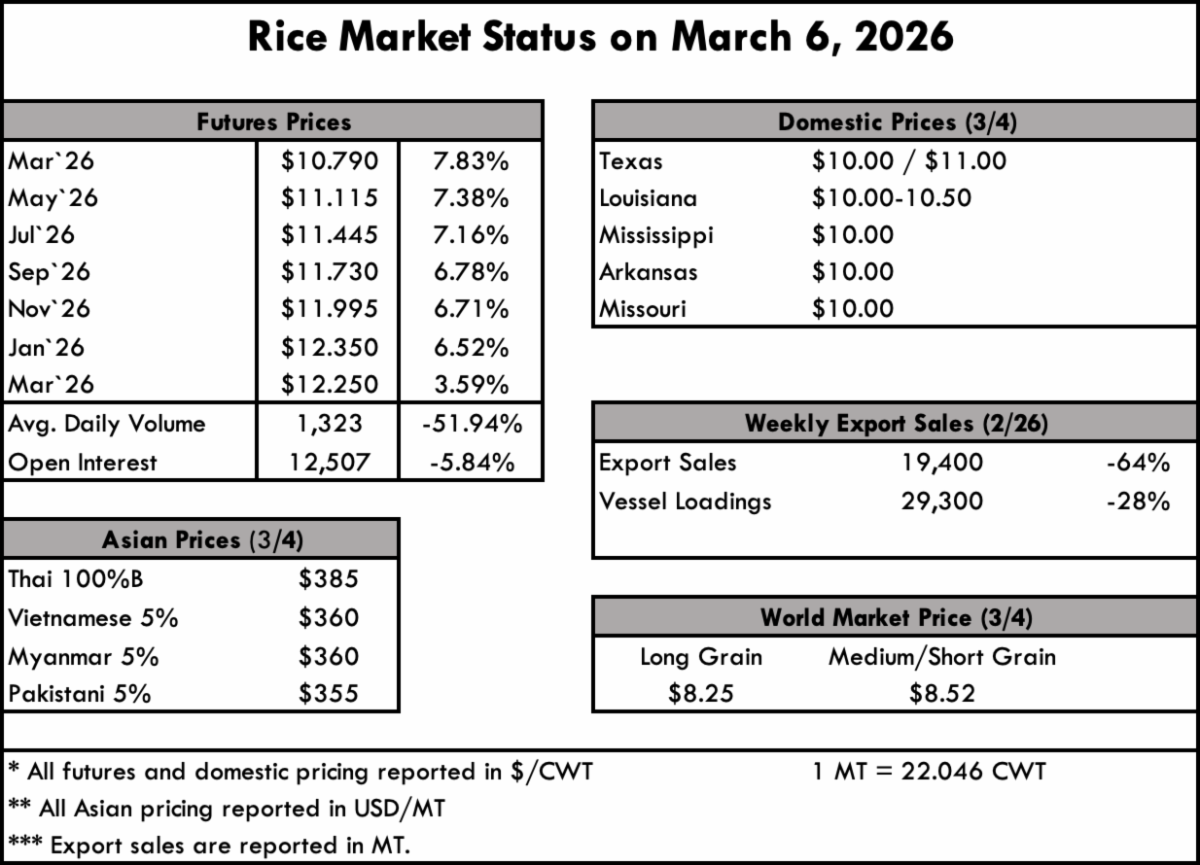

In Asia, there are reports of trade disruptions and payment issues, specifically between India and Iran. This is inevitable given the circumstances and will continue to multiply in the coming weeks. As of writing, it is difficult to analyze any direct impact pricing of the raw product of rice, but freight and logistics is certainly being impacted. Therefore, we will report rice prices as sideways out of Asia, with Thailand being $380 pmt, Vietnam at $360 pmt, and India at $350 pmt.

In South America, Brazil will play the decisive role in shaping regional rice trade over the next several weeks, as its import demand and buying patterns largely determine how rice moves within the MERCOSUR market. Brazil continues to be an outsized player in export channels in recent years, with exports reaching roughly 1.5 million tons in 2025. Paraguay remains the most vulnerable country in the region, carrying sizable old-crop inventories and relying heavily on Brazilian demand to clear stocks, which makes its market outlook closely tied to Brazil’s purchasing decisions. Argentina is transitioning steadily into harvest, with domestic consumption providing an important buffer that helps absorb early supplies and prevent immediate harvest pressure from weighing heavily on prices. Uruguay, by contrast, enters the new marketing year in the strongest structural position among the major exporters, supported by relatively low carryover stocks and disciplined forward sales coverage that reduces exposure to short-term market volatility. A new Brazilian paddy rice export subsidy for farmers is expected to be published in the Brazilian federal register today. The current Mercosur harvest is in full swing, and reports of an overall decline are mentioned to be somewhere between 8-15%. Mercosur exporters continue to be active throughout the Western Hemisphere.

The weekly USDA Export Sales report shows net sales of 19,400 MT, down 64% from the previous week and 74% from the prior 4-week average. Exports of 29,300 MT were down 29% from the previous week and from the prior 4-week average.

|

")