|

This week, the U.S. long-grain rice market remains cautious as the first seeds have gone in the ground in south Louisiana and likely somewhere along the Texas gulf coast. The carryover of 39 million cwt is like a wet blanket on the prices, with any producer holding physical rice unwilling to sell at current levels. While in many marketing cycles there are factors that can result in volatility, it is difficult to find any at the moment. Even with the anticipated acreage reduction of at least 25% for long grain acres overall, increased prices remain an uphill battle given the global supply dynamic. We would caution anyone hoping to speculate on medium grain acres as well, as California is looking to have a crop at least as large as last year (525,000 acres) if not larger. Significant storms on the west coast in the past week have secured the snowpack and reservoir flows to ensure a full plant, unless there are late storms that will result in prevent plant. Acres in the south will already be committed by then, however, so we can’t recommend speculating on medium grain as a sound marketing strategy.

Despite the weak outlook, it does appear we are bouncing along the bottom at this stage, and no longer in free-fall. Prices have largely stabilized at their current levels in both the Eastern and Western Hemispheres. The Mercosur region will be an extremely fierce competitor in the coming months, though, specifically Brazil and Uruguay where new crop harvest has started. Despite a reduction of approximately 8-10% overall in Mercosur, the market is slow, and a significant carryover of stocks will create tough competition. We understand a Brazilian government announcement of an export subsidy is forthcoming and should be formally announced at any moment. If we are fighting for market share in Mexico, other Latin American countries, or even the EU, markets that have been “secure” in the past aren’t guaranteed to be so moving forward. This is not a new revelation, but it does mean one must be prepared to compete for markets… which is another way of saying the price will remain cheap with stiff competition.

In light of these points, we are fortunate to retain a strong presence in Haiti and Iraq, both of whom continue to procure significant quantities of milled rice on a regular basis. The most recent success with the Colombian TRQ is also buoying the sentiment at the mills for throughput but is still too lackluster to ignite a shortage of supply.

Taking a look at Asia, prices are right in line with where they’ve been for the last three months. Thailand has bene holding firm at $390 pmt, with Vietnam closer to $370 pmt. India, as expected, rests at $360 pmt, setting the tone for the depressed prices worldwide. The spread between the Asian origins and U.S. long grain has been shrinking over the last three months, but unfortunately because U.S. prices have been converging on Asian prices, not the other way around. U.S. Long Grain milled rice quotes reside at $530 pmt right now, higher than Uruguay and Brazil by around $80/ton, but U.S. rice holds a freight advantage to many customers.

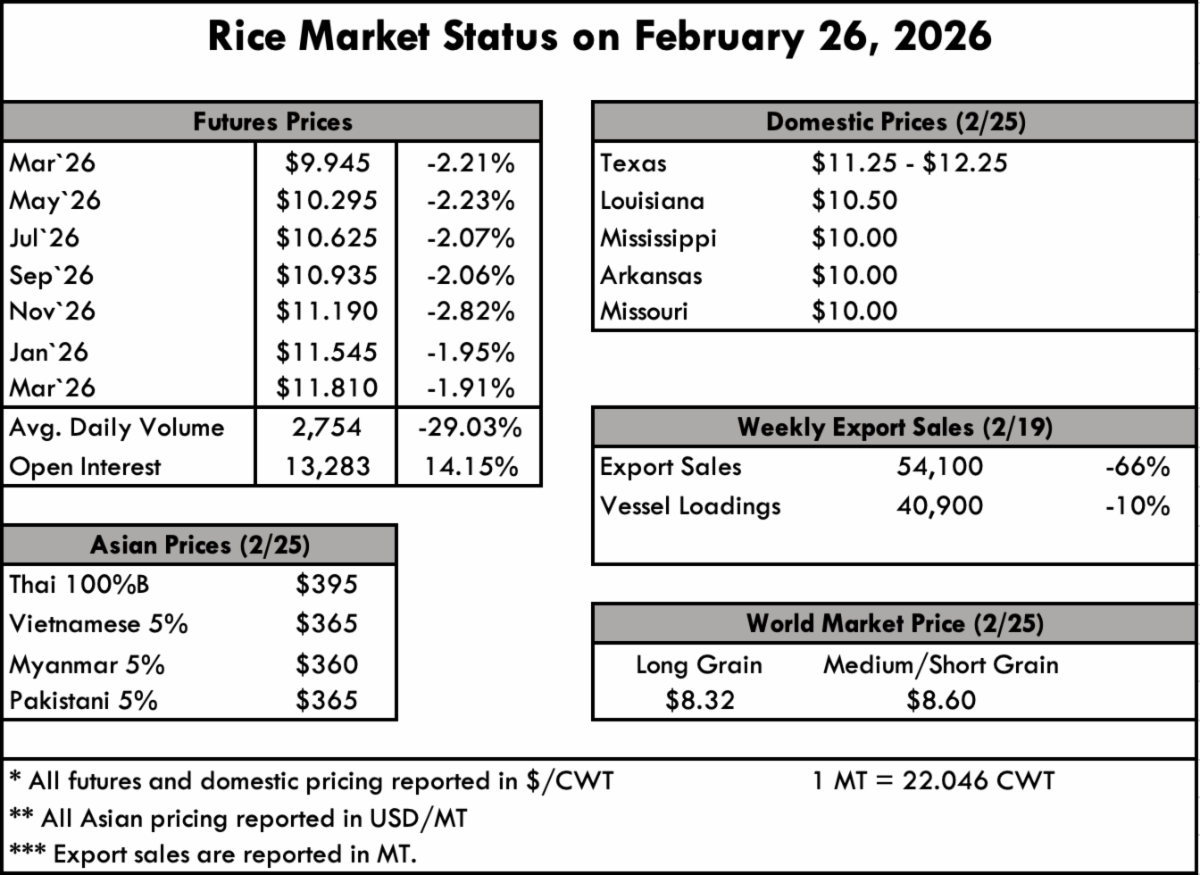

The weekly export sales report shows net sales of 54,100 MT this week, down 66% from the previous week and 30% from the prior 4-week average. Increases were primarily for Colombia (16,000 MT), Haiti (15,200 MT), unknown destinations (12,000 MT), Mexico (5,500 MT, including decreases of 100 MT), and Honduras (1,000 MT). Exports of 40,900 MT were down 10% from the previous week and 21% from the prior 4-week average. The destinations were primarily to Panama (18,800 MT), Japan (13,600 MT), Mexico (4,800 MT), Canada (2,300 MT), and Taiwan (800 MT).

|

")