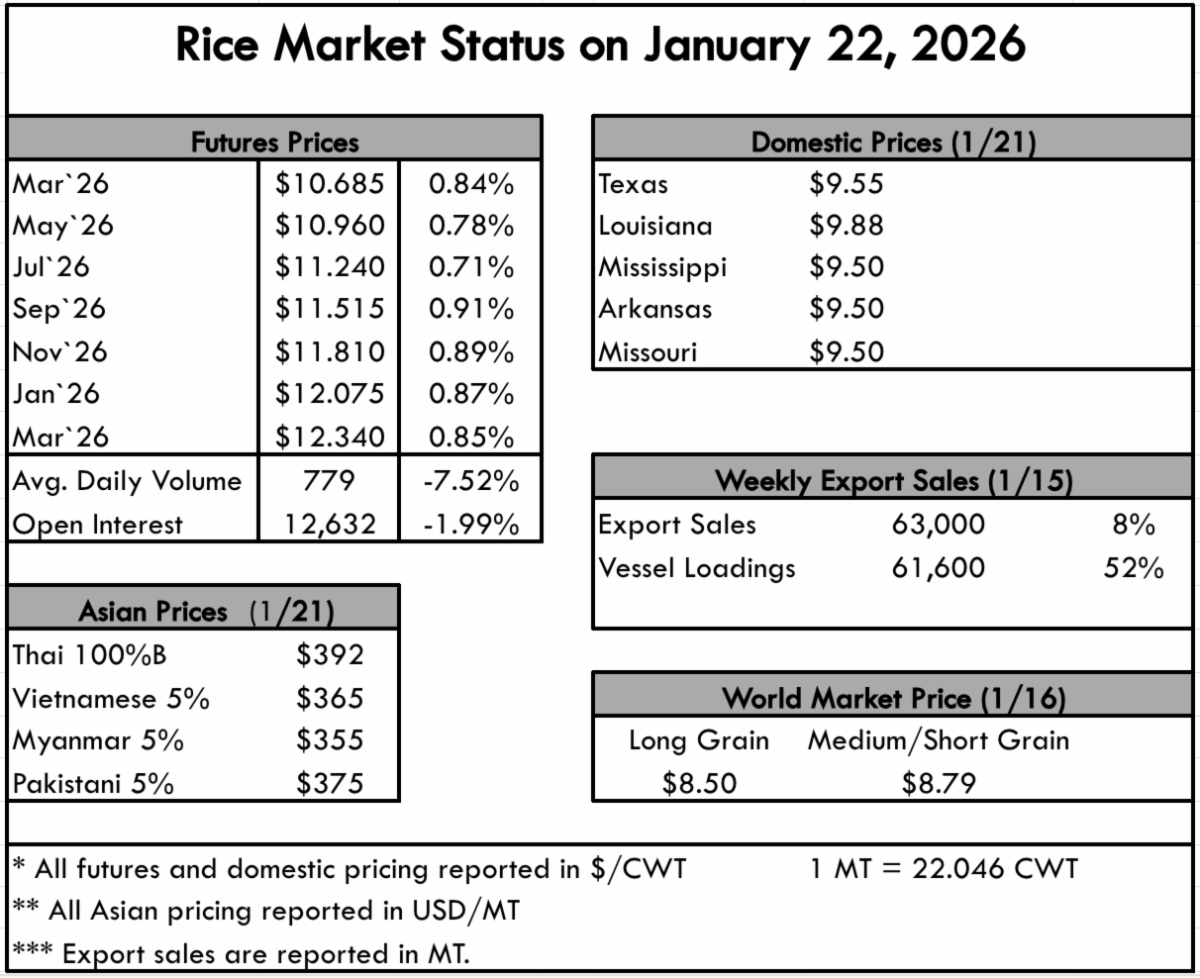

|

The most recent FAO report from December is in, and the FAO All Rice Price Index (FARPI) rose for the first time in several months! It jumped up 4.3% from November to December but is still 15.2% below the same time last year. Glutinous rice was the big winner and the primary reason for the increase, but Thai rice also saw some stabilization. Thai rice was buoyed by the price stabilization measures and G2G sales agreements that were announced in November. All told for 2025, the small uptick in December couldn’t overcome the downward slide the FARPI tracked, finagling out at a 35.2% skid from 2024. Indica dropped the most at 38.4%.

One difficulty in a market environment this dismal is that even good news gets brushed under the rug. Things like Thai prices being 13% higher this month than they were in October would normally be celebrated, but when the October price was a decade-record low, it’s hard to get too excited. That sentiment carries into the U.S. long grain market, where some signs point to us maybe approaching a turning point, but it’s so bad it’s hard to be optimistic. Milled prices remain at $575 pmt NOLA, with some reports dropping as low as $550 pmt. But with signs beginning to show that other origins have stopped their freefall, the U.S. may be in position for a turnaround. Most of the Mercosur has liquidated their old crop stocks, except for Brazil. Brazil’s old crop stocks are hanging like a wet blanket over any upward movement. New crop harvest is underway in Paraguay, but it is not in full swing yet. The same goes for Brazil, with Argentina and Uruguay harvests approaching. In general, this harvest is reported as in good shape after a 5-8% reduction in acreage.

The sharp reduction in planted acres expected for this year’s U.S. crop will certainly help from a supply perspective, but the quality will have to answer as well. Rice crops will be susceptible to climate risk as always, but we implore producers to use discretion in what fields and what varieties are planted. The variety sprawl has created a structural quality problem that has become endemic in the industry. By cutting out 30% of the acres, it would be our hope to reduce the varieties planted and harvested, thus delivering a more consistent product to the mill and then the consumer. This is exactly what the South Louisiana Rail Facility has been able to accomplish and consistently receives premiums for its product. There has also been considerable discussion of mills contracting jasmine rice acres with farmers along the Gulf Coast and throughout the delta. Variety, seed availability, pricing, and anticipated field yields are under assessment.

USRPA is actively engaged in the fight to secure more funding to help close the gap beyond what the FBA was able to accomplish. Rice producers, after ECAP and FBA payments, are still losing over $210 per acre due to unfair trade practices from our global competitors. We commend Senators Boozman and Hoeven for their expanded assistance proposal announced last week (more on that in today’s D.C. Update).

|

")