|

Does a ceasefire mean the Iraqi vessels can discharge U.S. rice? This is the biggest question on the minds of exporters right now, as there is one fully loaded vessel anchored in the Gulf waiting to discharge, and there is another booked vessel scattered on barges still in the U.S. waiting to be loaded. This hiccup in the supply chain causes a chain reaction down the line and ends squarely back in the producer’s pocketbook. Not being able to realize the disappearance of rice, despite the demand being there, only prolongs the depressed pricing situation.

On the supply side, the “bright” spot is the 30% reduction in acreage reported by the USDA. With fertilizer and input costs continuing to rise due to scarcity and logistical nightmares, it only provides further incentive to not plant rice but choose an alternative crop with significantly lower input costs.

While these are the two “headliners” at the current moment, there remains steady domestic business, milled business to Haiti, and paddy exports into Mexico. South America is certainly a strong competitor, but the hope is that the reduction in supply from the U.S. long grain sector will help shore up prices when we get deeper into the year. The competition with South American origins is very real, however, and could have lasting implications if current conditions persist. The Mercosur harvest is currently 50% completed if not more. In general, reports are that yields are slightly lower, but grain quality is excellent with regards to milling yields and chalk.

On the West Coast, producers are all working their ground getting ready for planting, but there are intermittent weather systems moving throughout the Sacramento region. There was a minor storm registered last week, but a larger one expected this weekend and early next week that is forecast to drop 1”-2”. The larger context here, however, is that snowpack is at 0%, while reservoirs are full. This is extremely abnormal, and the belief is that full surface water allocations this year simply means borrowing from next year. Pricing remains difficult and well below break even for medium grain producers. The California medium grain crop is expected to exceed 530,000 acres, barring a late and extreme weather event.

The FAO Rice Price Update for March shows the FAO All Rice Price Index (FARPI) reducing by another 3%, which is 3.8% below these levels last year. We predicted this per the last FAO report, as there was no letting up on the global supply of rice and India’s bulging stocks that have resulted in dumping rice across the globe. Prices don’t have much more to fall, and with the fertilizer crisis in our midst, it is already expected that global yields for rice and other crops will be off at least 3-5% in the coming year. The FAO reports that 11% of globally traded rice volumes transits to the Persian Gulf countries, and the current conflict has certainly impeded those flows.

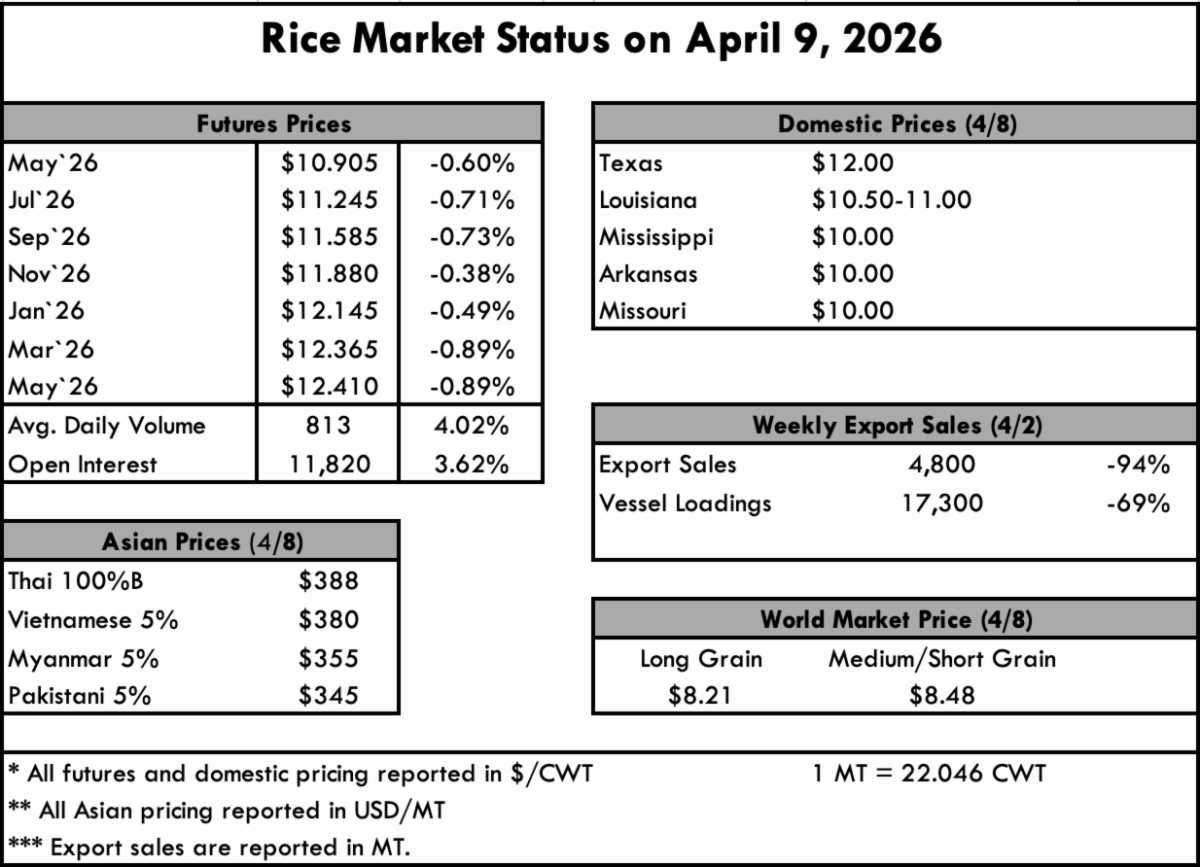

In Asia, prices have firmed in Thailand and Vietnam, with quotes being as high as $380 pmt in Thailand, and the same for Vietnam. This is up significantly from last report for both origins. India remains low at $340 pmt where we are told some 57 million tons of milled rice is in storage largely due to the inability to service Middle East ports paralyzed by the war conditions. U.S. #1 long grain is quoted at $550 pmt for indicative purposes.

|

")