|

Last week we had a thorough discussion on expected long grain acreage reduction in the coming year. We had plenty of feedback, some positing the decrease will be a minimum of 30%, while others projecting a maximum of 20% long grain reduction, particularly in long grain. Whichever the case may be, it can be decided that at least one-fifth of the crop will not get planted next year, and this should be viewed as an opportunity to hone in on quality varieties that produce strong milling yields and help liquidate old crop carryover that will significantly absorb any reduction. A few farmers in south Louisiana will be putting seed in the ground early next week assuming weather permits.

From a global perspective from the WASDE, global rice production is slightly higher from last month, primarily due to an increase for Cambodia. Global trade is virtually unchanged with increases to Burma, China, and Tanzania exports nearly offsetting a reduction for Thailand and the United States. Global consumption is down on a reduction to Burma, more than offsetting increases for China, Japan, United Arab Emirates, and Cote d’Ivoire. Global stocks are forecast higher due to Thailand, Burma, and Cambodia.

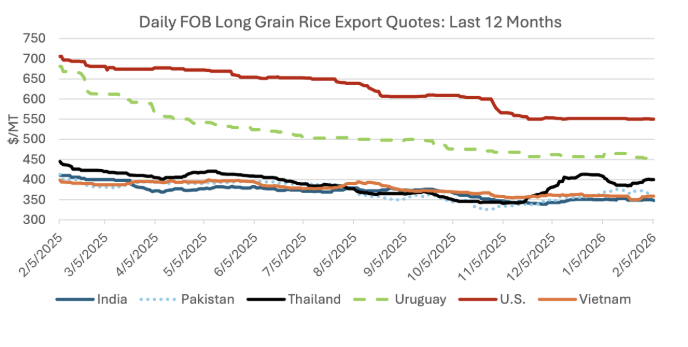

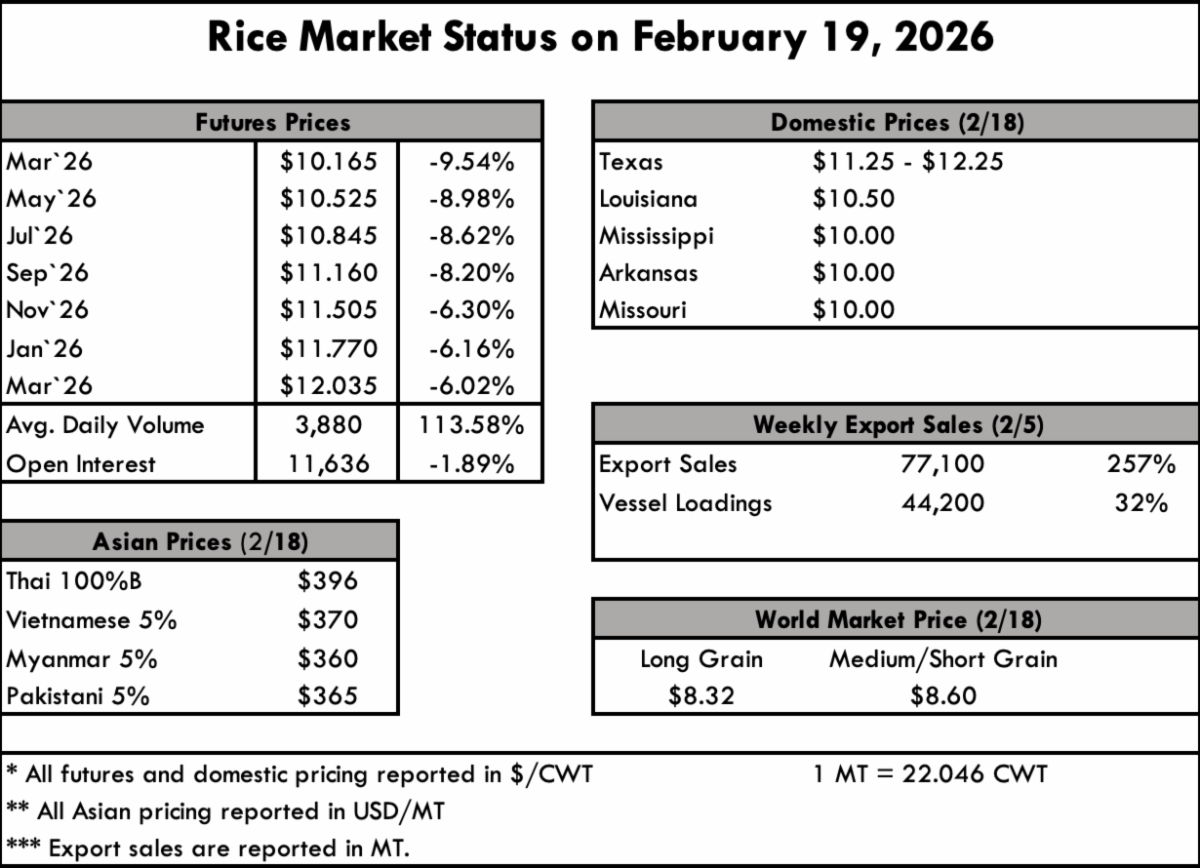

Since the January WASDE, global export quotes decreased aside from Thailand. U.S. quotes dropped $2 to $550/ton on continued weak sales to Latin America. Uruguayan quotes declined $13 to $453/ton as customers wait for the harvest of the new crop. Indian quotes are down $3 to $351/ton. Vietnamese quotes decreased $1 to $359/ton despite sales to the Philippines resuming following the expiration of the temporary rice import ban. Pakistani quotes dropped $4 to $366/ton, reflecting reduced demand from core Middle East markets. Thai quotes were up $4 to $400/ton, on currency appreciation, and are the highest among major Asian exporters.

|

")