|

It’s official: the Iran war hurts and is leaving its mark on the U.S. rice industry. The Western Hemisphere trade gets the lion’s share of U.S. exports, but with that market waning in recent years, business with Iraq, Saudi, Qatar, UAE, and other destinations in the Middle East have become increasingly important outlets. That has come to a screeching halt with the Port of Hormuz closed, and no indication of when it will be opened. The recent tender awarded to Iraq is on hold, and sending reverberations through the industry here, where barges can’t be loaded as there’s no way to get the rice to Iraq.

We can look back only a few years ago when the Houthis bombed Israel on October 7, 2023. That resulted in the closing of the port in Yemen, a major discharge point for Calrose rice into the MENA region. Consequently, California exporters began stockpiling rice that couldn’t be shipped (despite there being demand), and the on-farm pricing dropped nearly 20%. The situation was eventually resolved, but not without detrimental impacts to the local farming community and long-term Calrose customers. We can expect to see this story repeat itself, but this time to the long grain farmer in the South. There will be pent up demand in the region when the Strait reopens, but it won’t entirely undo the damage being done in the current moment.

The U.S. long grain planting season has lost additional acres due to the increased costs of production in the form of higher oil prices and their effect on fertilizer, ag-chemicals and fuels in general. The March 31 USDA Planting Intentions Report should give us a good indication of reality and the % drop from previous years. The actual plantings report comes out on June 30.

In South America, the first supplies from the new crop are finding their way into the market. Given that there are no drastic changes in expectations, pricing remains fairly consistent. This isn’t particularly good news, as pricing is already well below break even for U.S. producers, but competition will remain in the coming months, particularly with Uruguay, and then Brazil. Competition will be especially fierce in the paddy market, where the quality from the U.S. crop is no longer preferred, and demand is shifting to alternate Mercosur origins. The Mercosur harvest continues throughout the four countries where acres are down approximately 10% from a year ago.

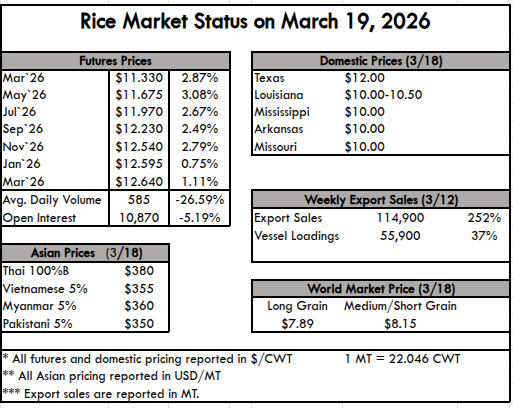

In Asia, new crop supplies from Thailand will begin putting even more pressure on an already depressed complex. Currently, prices in India remain at $355, steady for nearly 90 days, and the same for Vietnam. Thailand has seen the most variability, with quotes at $375 pmt this week.

The weekly USDA Export Sales Report shows net sales of 114,900 MT this week, up noticeably from the previous week and up 72% from the prior 4-week average. Increases primarily for Japan (65,000 MT), Honduras (23,200 MT), Mexico (13,700 MT), and Haiti (7,200 MT). Exports of 55,900 MT were up 37% from the previous week and 43% from the prior 4-week average. The destinations were primarily to Honduras (22,400 MT), Japan (13,500 MT), Mexico (5,600 MT), Guatemala (5,400 MT), and Canada (2,100 MT).

|

")