")

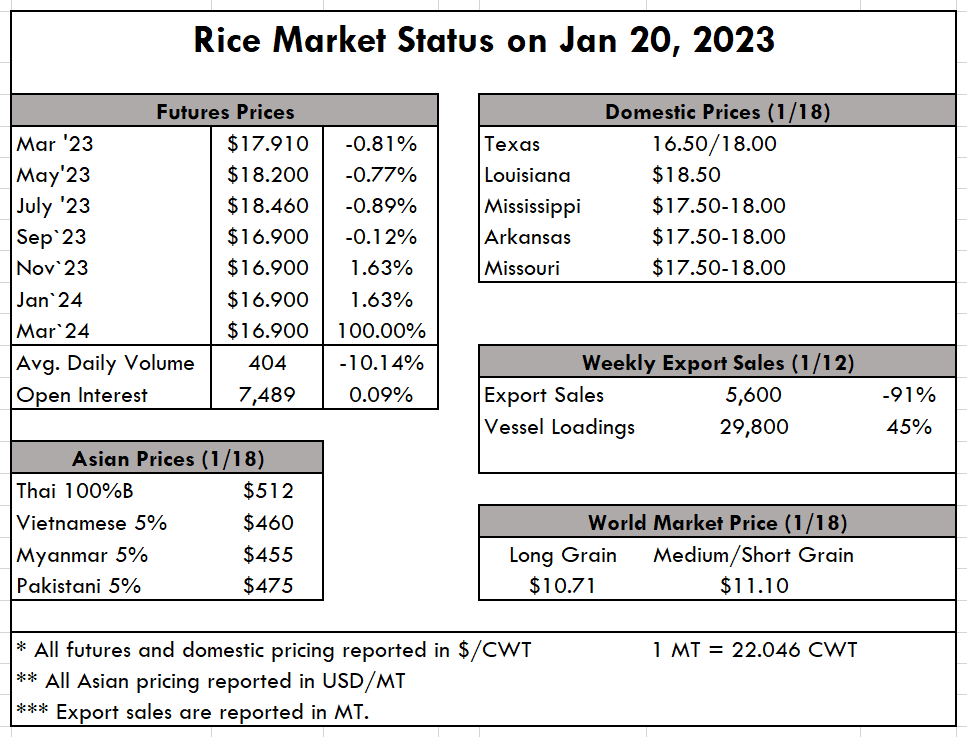

| Planting intentions are officially on the minds of rice producers and the “holiday fog” is lifting off the market. To begin, an unprecedented offer for medium grain surfaced last week, where one of the larger coops in the south procured approximately 60,000 acres of medium grain at prices in the $20/cwt range. This is a very rare occurrence indeed, and it now appears that medium grain seed will be the constraining factor for more growth in acreage. The move to medium grain would make sense for growers in the South, especially when considering the enormous reduction in California production this year, and the resulting record pricing in excess of $1,600 pmt that Calrose has experienced. A spike in medium grain acres in the South is to be expected though, as the ERS Rice Outlook points out that last year only 398,000 total acres of medium and short grain were harvested in the U.S. This is 28% fewer MG/SG acres than the previous year, and the lowest since at least 1972/73. Read more here. The long grain market continues to be a head-scratcher; export demand remains low while prices are high. The high prices are on account of a short crop, but when compared to other origins, U.S. rice is well over $200 pmt higher than its competitors. We reported last week the excellent news of an additional 44,000 metric tons of business to Iraq, and the significance can’t be understated when the country could have sourced that rice from Thailand at prices closer to $500 pmt. All this to say, the export business is more than welcomed and helps complement a steady core of the domestic business that has held the market firm all year. We eagerly await more news on planting intentions in the coming weeks as producers evaluate bean and corn prices, and how those will work into crop rotations this year. In Asia, Thai and Viet prices have officially separated from Indian prices. This is the result of strong demand in the new calendar year, available supplies, and currency fluctuations. But one thing we expect is to see these bifurcated markets converge a bit more in the coming weeks and months. Expect to see the Indian prices creep up from their current levels just below $400 pmt, or Viet and Thai prices soften from their current levels of $455 pmt and $495 pmt, respectively. We will turn now to Brazil, the emerging and most significant threat to the Mexico and Central American markets. A report published this week by ABIARROZ, the Brazilian rice organization, highlights that milled exports have returned to pre-pandemic levels in volume, and have surpassed those levels in value. Milled rice accounted for 52.4% of total rice exports in value, a drop from previous years, but paddy rice exports reached their highest levels both in volume and value, respectively 98% and 75% higher than average. Reports of drought in the region will certainly impact production and exportable supply, but will nonetheless have an impact on the U.S. long-grain complex. As mentioned in last week’s RA, the long grain trade is looking towards the results of the Colombian tender on January 23 that calls for 89,779 tons (milled basis) or the equivalent in paddy. This result will be a good measuring stick for where the US export outlook. |