| Rice Farmers Need Favorable Prices |

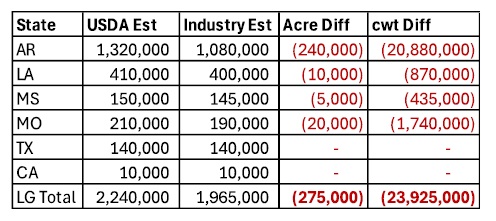

| There has been growing frustration in the market over delays in USDA reporting, and the impact this is having on pricing is substantial. This year in particular, planted acreage estimates appear to be significantly overstated, placing heavy pressure on prices for paddy rice still in first hands. To bring more clarity, we’ve surveyed planting expectations across key rice-producing states and taken a conservative but realistic approach to estimating total long-grain acreage losses. In reality, the shortfall could be even greater. |

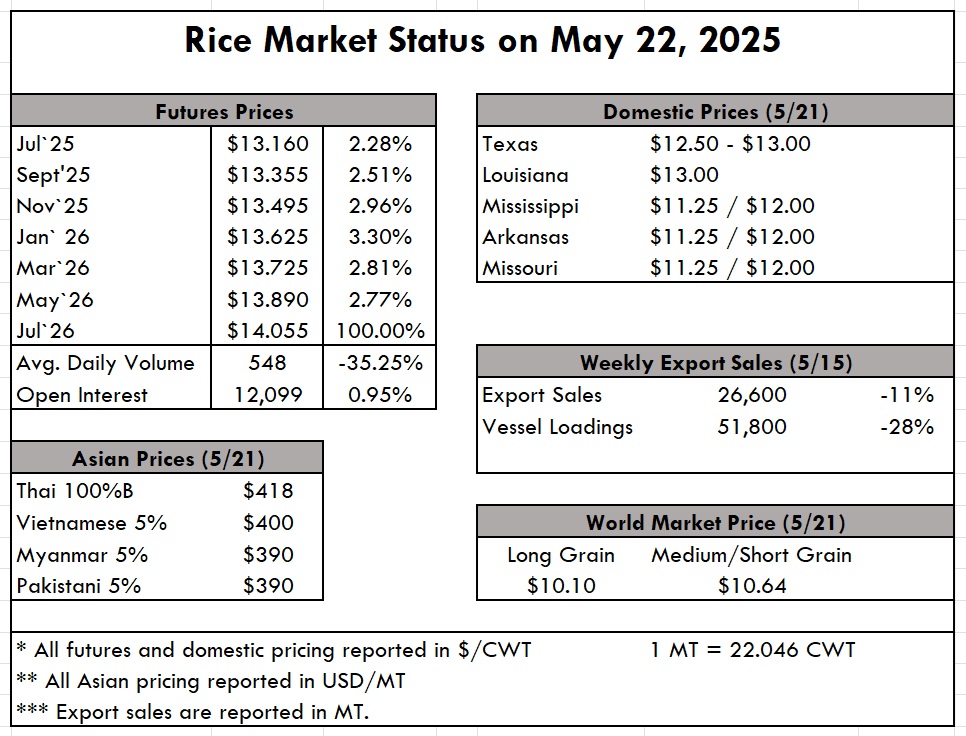

As the table illustrates, by not adjusting for lost acreage in this month’s WASDE, current production projections are overstated by at least 275,000 acres, or roughly 24 million cwt. This disconnect is materially affecting growers still trying to sell and mills attempting to manage inventory. While the true numbers will eventually surface, for many, it may be too late to influence favorable pricing. As the table illustrates, by not adjusting for lost acreage in this month’s WASDE, current production projections are overstated by at least 275,000 acres, or roughly 24 million cwt. This disconnect is materially affecting growers still trying to sell and mills attempting to manage inventory. While the true numbers will eventually surface, for many, it may be too late to influence favorable pricing.With planting largely in the books and on par with the four-year average of 87%, we turn now to initial crop quality reports. As of the May 18 USDA report, 28% of the overall rice is rated Excellent, 51% rated Good, 18% Fair, 2% Poor, and 1% Very Poor. It’s still early to place too much stock in these numbers, but a positive sign that nearly 80% of the crop is rated Good or Excellent. In Asia, market conditions remain soft. Demand out of Indonesia has cooled, pushing Indian prices as low as $385/MT, with Vietnam and Thailand holding around $400/MT but showing little upward momentum. Iraq continues to fulfill its MOU obligations with U.S. suppliers despite the pricing disadvantage, driven largely by geopolitical ties. Iraq is now the second-largest buyer of U.S. milled rice, trailing only Haiti. There are encouraging signals that Iraq may remain a consistent buyer in the coming years, though formal G2G agreements are still pending. This week’s USDA Export Sales report shows net sales of 26,600 MT, down 11% from the previous week and 29% below the prior 4-week average. Exports totaled 51,800 MT, down 28% from the previous week and 4% from the 4-week average, reflecting the broader slowdown in market momentum. |

|

25722 Kingsland Blvd., Ste. 203, Katy, Texas 77494

Phone: 713-974-7423

USRPA does not discriminate in its programs on the basis of race, color, national origin, gender identity, sexual orientation, religion, age, disability, political beliefs, or marital/family status. Persons with disabilities who require alternative means for communication of information (such as Braille, large print, American sign language, language translation, etc.) should contact USRPA at 713-974-7423. EEO.