")

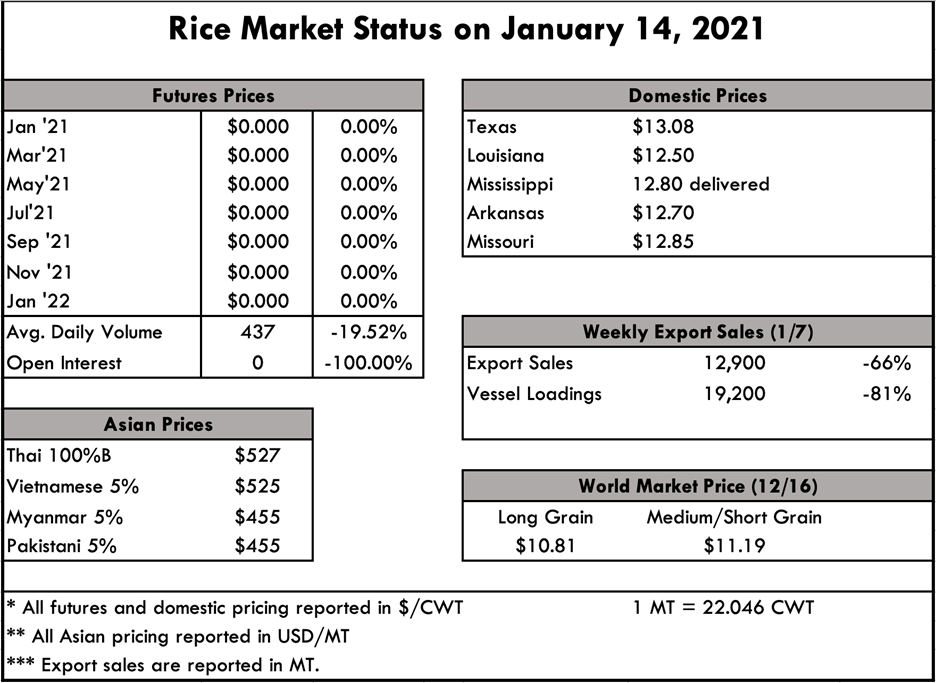

The spot market throughout much of the delta remains quiet. While rice continues to lightly trade, the market is lacking any significant developments that would cause prices to come off their month-long pricing. In conducting this week’s surveys, there appears to be minimal to no change in spot pricing from the early December trades. The cash market is expected to strengthen in the weeks ahead as the fundamentals reported in the most recent WASDE report work their way into the industry, which is already being seen in the futures market.

This week the USDA published their January World Agricultural Supply and Demand Estimates report which was generally accompanied by a more bullish undertone for grains across the board. These revisions quickly worked their way thru the futures markets where beans, corn, wheat and rice all posted respectable gains following the report’s release. The USDA elevated its production figure for long-grain rice, which was more than offset by a considerable uptick in domestic demand expectations. The latest demand forecast calls for a record 125 million cwts of domestic use, up from the historical average of roughly 108 million cwts. According to the USDA, this revision is the result of higher use during August and September as implied by the NASS Rice Stocks report. Ultimately this change pushed ending stocks down to 26.3 million cwts from the 38.2 million cwt projection a month earlier. Now the current ending stocks projection falls in line with the 10-year average. The USDA also bumped the season-average farm price for long grain by $0.20 per cwt. As for US medium and short-grain, the changes made to the balance sheet were unremarkable.

The USDA also published their Crop Production Annual Summary report which shows the final acreage figures for all rice in the USA. Last year’s bull market certainly bought more rice acreage, as the official data indicates long grain harvested acres were up 572,000 acres or 33% from 2019/20. Although Southern medium grain acreage was off by 72,000 acres in 2020, a strong Calrose market motivated growers to increase plantings which was reflected in the 2.6% year over year increase for the state.

Perhaps more noticeable than the increase in planted area were the yields. While yields in Arkansas, the nation’s largest rice growing state held steady year over year, the rest of the Delta benefited from cooperating weather and other factors that ultimately drove up yields basically across the board. As a result, total production was over 36% in 2020.

Looking to Asia, prices appear to have found a footing as all origins are up from 4-weeks ago. Pakistan export prices saw the sharpest increase, up $50 per ton from the prior month, while the appreciation in the other Asian origins was closer to $20-30 per ton for the same time period. At present, one of the more critical factors in terms of global trade pertains to container availability and costs. For the past 6-8 weeks, exporters around the world have struggled to find equipment and capacity to ship bulk goods. Due to this bottlenecking, shipping and logistic prices have spiked to 52-week highs, making trade especially difficult in certain regions.

According to the International Grain Council (IGC), which publishes a price index for soybeans, corn, wheat, barley and rice, prices are up 10.3% from a month earlier, and 37.9% from a year earlier. The commodities posting the largest gains are soybeans up 10.9% and corn up 13.4% this month.

As expected, these fundamentals are now being reflected in Chicago, where futures prices continue their march upward. Most analysts have published various comments surrounding the bullish undertone taking shape in the market. With planting right around the corner, significant price action at the futures level could certainly have a large impact in what gets planted this spring. Typically, when a price hike is accompanied by rising volume and open interest, the market is considered strong, which is exactly what we see happening in the market right now. Between a new administration entering the office, ongoing currency volatility, shipping & logistic constraints, and projected plantings, there are multiple variables coming to bear on the market over the next several weeks that could perpetuate the market strength or reduce it; for these reasons, it’s important to maintain market liquidity in order to reduce price risk.