")

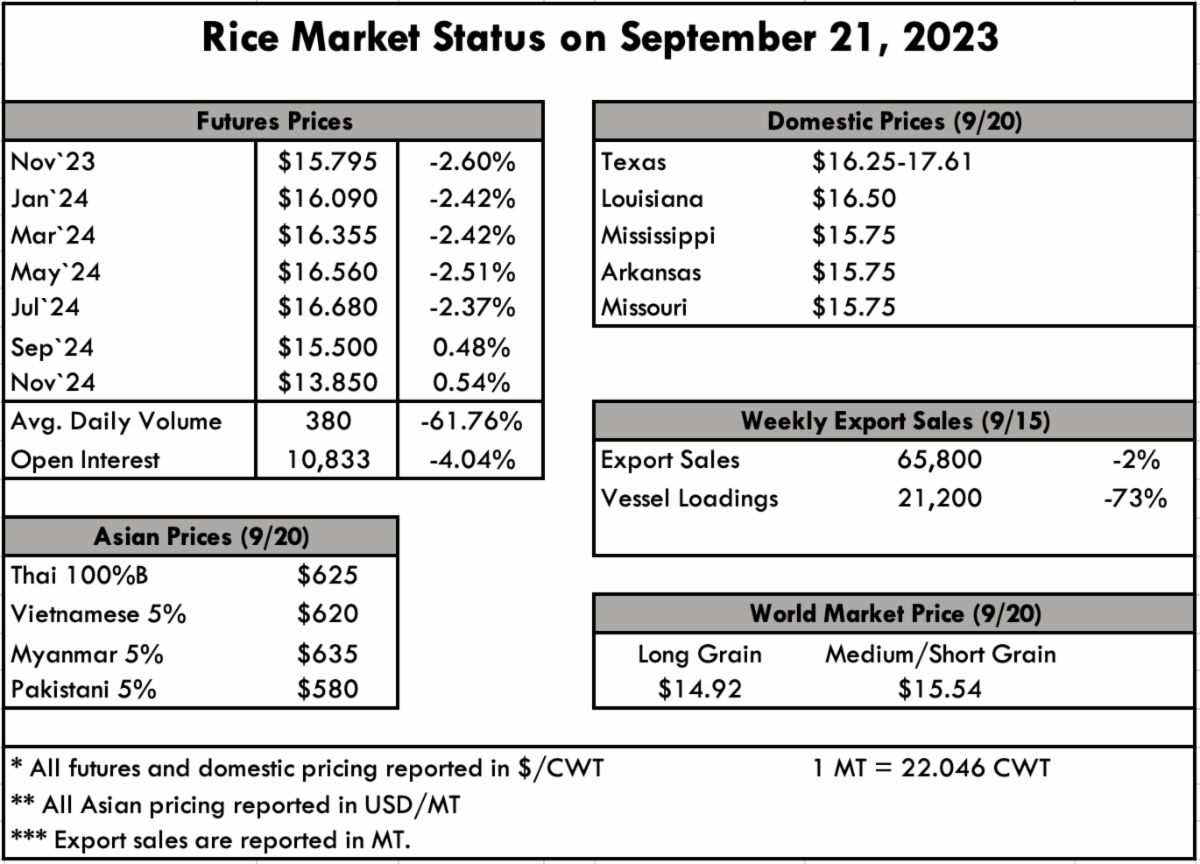

| Is the story for this marketing year already written for the U.S. long-grain crop? One could argue that it’s all but over before harvest is even finished. Every year has unique features, and this year is punctuated by the Indian ban and the resulting scramble that has gobbled up a bumper crop, and all but made a bearish WASDE report that increased paddy by more than 6 million cwt a mere speed bump in the wake of strong demand. Last year when prices were steady at $680pmt for the back half of last year’s short crop, the expectation was that this year’s large crop would make U.S. long grain more competitive, and prices would drop to converge with South American exporters. However, a strong market in Iraq and Haiti, bolstered by steady domestic business, has firmed prices even further, while South American export prices race upward to converge with U.S. prices — now finding rest at a minimum of $700pmt. We can confirm one sale of Uruguayan milled rice at $760/ton FOB Montevideo destined for Peru. We would contend that the dust is settling from the Indian situation, and we have a steady market moving through the first quarter of 2024 at this juncture. We know that export prices are firm, and cash prices are looking the same. Texas is seeing cash prices of $16.25-$17.61/cwt based on preferred variety and quality of milling yield. Louisiana is looking at $16.50/cwt, while Mississippi, Arkansas, and Missouri are at $15.75. The crop progress report shows steady movement toward completion, with California finally underway in a meaningful way, though still at only 6%. Arkansas is now 15% above the pace for the 5-year average, crossing the halfway point and sitting at 58%. Louisiana and Texas are at 93% and 90% respectively, while Missouri is at 27% and Mississippi is at 74%. The weather is favorable, and much still depends on milling yields to determine just how far this crop will go. Early milling yield reports continue to be very inconsistent, “mostly in the low 50s.” Prices are settling significantly in Asia, where only weeks ago they exceeded $650pmt, but are now reported at $625pmt for Thai rice and $620 for Viet rice. Myanmar and Pakistan are at $635pmt and $580pmt respectively. A recent GAIN report on Vietnam shows rice exports surged to 656,869 tons in August, with the primary markets being the Philippines, Indonesia, Ivory Coast, Ghana, and China. The Philippines jumped 45% from the previous month and accounted for 36% of all of Vietnam’s exports. This surge could be in response to the Thai government encouraging its rice farmers to plant less water-intensive crops as El Nino is impacting the moisture cycles. The weekly Export Sales report registers net sales of 65,800 MT, down 2% from the previous week, but up 24% from the prior 4-week average. Increases were primarily for Mexico (28,100 MT), El Salvador (12,000 MT), Honduras (10,000 MT), Saudi Arabia (8,600 MT), and Israel (4,000 MT). Exports of 21,200 MT were down 73% from the previous week and 58% from the prior 4-week average. The destinations were primarily to Saudi Arabia (8,800 MT), Guatemala (5,500 MT), Mexico (4,900 MT), Canada (1,600 MT), and the Bahamas (100 MT). |

|