")

This week, the USDA released the December WASDE report which contained only minor revisions for both U.S. long-grain and medium & short-grain. The USDA didn’t make any notable changes to the 2020/21 balance sheet in this report but rather focused on the 2021/22 crop. Long-grain imports were revised downward, while export and domestic demand was left steady from the November report. Ultimately, the 2021/22 long-grain carryout was lowered by 1 million cwts, entirely the result of lower imports. Season average farm prices improved, but only slightly, up $0.10 per cwt to $13.10.

Medium & short-grain imports were also lowered this month, but that was more than offset by lower export use which is attributed to higher prices and less supply. The domestic use, as per the norm, appears more resilient against the current market conditions and is even expected to exceed last year’s demand. Ending stocks were assessed up 500,000 cwts, and while California’s price projections are unchanged from last month, southern medium-grain was lowered $0.30 per cwt to $13.70 per cwt.

On the ground, there is little to report in the way of cash trade activity. With tax implications prohibiting some from selling, and the normal holiday slow-down inhibiting others, a more mellow pace is normal for this time of year. However, the market is abuzz with what next year’s acreage numbers will look like as a result of the soaring fertilizer costs and the potential for growers to plant more corn and beans. The expectation is that the largest reduction will come for Arkansas and that Louisiana will remain close to the same as this year. Mississippi and Texas are still up in the air, and California acreage on the West coast is completely contingent on precipitation and the ensuing water policy.

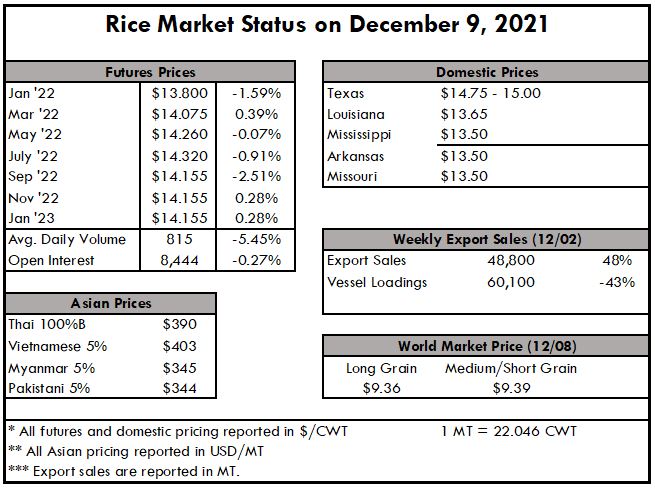

In Asia, prices remain relatively constant. Thai rice remains around $385pmt, Viet at $405pmt, and Indian down at $355. It is notable that Viet prices have dropped in recent weeks to come more in line with Thai prices, while Indian rice has held steady along with their record-breaking export pace.

The weekly Export Sales Report shows net sales of 48,800 MT, which is up 51% from last week, but down 22% from the prior 4-week average. Increases were primarily for Honduras (18,500 MT), Guatemala (13,100 MT), Jordan (4,100 MT), Taiwan (3,000 MT), and Canada (2,400 MT).

Exports of 60,100 MT were down 42% from the previous week and 21% from the prior 4-week average. The destinations were primarily to Guatemala (14,400 MT), Japan (13,000 MT), El Salvador (12,400 MT), Haiti (12,400 MT), and Canada (2,600 MT).

Futures have been taking a hit since Thanksgiving, with the low registering this week at $13.79. This could be on account of the cash market being slow, the typical slow-down this time of year, or simply the difficulty in the logistics sector. Average Daily Volume is 815, down 5%, and Open Interest is at 8,444, holding even with last week.